If you are an operator or are responsible for Finance in a startup or a scaleup that has recently secured funding, your primary concern is likely not running out of cash. Instead, you're focused on putting it to good use in the most efficient way possible. Deeply understanding your cash flow and how market dynamics might work for and against you is a core part of your day-to-day job in the finance team.

In this article, we’ll explore how interest rates affect startup capital and access to funding, how to understand the impact interest rates have on your business and how to optimise your cash flow management process to stay ahead.

How do interest rates impact your cash flow?

Higher cost of capital: Businesses, particularly startups and SMEs, require financing to fund their growth and as money gets more expensive companies begin to feel the heat if those growth ambitions aren’t realised. If borrowing gets too expensive, there is generally a renewed focus on optimising working capital in an effort to fund growth internally.

Purchasing power grinds to a halt: As inflation and interest rates rise, individual and organisation spending power decreases. Whether you are a B2B or B2C/D2C business, you will notice your monthly sales numbers being impacted and will need to act accordingly by revisiting and paring back that over-optimistic budget you set last year.

Pricing pass-through: Interest rates push the price of goods and services up which leads to suppliers and vendors increasing their wholesale or retail prices to protect their margins, meaning your marketing dollar efficiency decreases, distribution to your customers becomes more costly and your annual costs for your tech stack rise meaningfully.

How can you adjust operationally to thrive in such an environment?

Unfortunately, there is no golden bullet to protect you from the risks of high inflation and expensive debt. There are a few tips however that we believe will give you a fighting chance at survival.

Optimise for cash conversion

Start by doing a thorough audit of your current cash inflows and outflows. Chances are you will be able to reduce or optimise your cash conversion cycle to free up some cash to cover your working capital or build a contingency fund. As part of your audit, review your existing creditors and negotiate lower interest rates or payment terms if possible.

Be vigilant about forecasting

Improved visibility around cash flow forecasting allows you to anticipate potential changes in your cash flow and modify your strategy or operating model accordingly. By accurately predicting future cash flows you can take proactive steps in the moment to pivot your business model and cash strategy if the landscape you operate in changes abruptly. Doing something as simple as preparing and reviewing a 13-week direct cash flow forecast can certainly help in the short-term.

Hedging can be for everyone

If you have contracts or financial instruments that commit to deliver cash flows at some point in the future but there is material risk based on movement in the market to that delivery, exploring a cash flow hedge (a derivative) can lock future values in.

Invest in cash flow management software

Viewing, managing and understanding cash flow is a full-time job. It gets harder and more complex as a business expands into new markets, grows its cost base, opens new bank accounts and invests in capex projects. By implementing a centralised system that integrates your financial platforms (banks, PSPs, ERPs etc) to consolidate, track and understand the granular levels of your businesses cash flow, you can promote a cash flow culture and prioritise the financial health of your business.

It’s important to remember that no strategy is a 'one-size-fits-all'. What works for one business may not work for another, and each strategy must be tailored to meet your business model and unique circumstances.

If you can't measure it, you can't manage it

This statement is particularly true during times of economic volatility. A fundamental aspect of efficient cash management is the ability to track and accurately measure cash flow movements and quickly respond when metrics start trending the wrong way. Remember, it is those companies that think deeply about cash flow and cash preservation through times of market uncertainty that come out the other side in great shape and ready to thrive.

Consider using Payable - it's a cash reporting and cash flow forecasting tool that connects banking and finance data to a central dashboard in real-time. Finance teams can track their cash positions across multiple accounts, currencies and entities and act fast when to move their metrics in the right direction.

Financial Automation

07 Aug 2024

Prior to launching Payable, I built platform and marketplace payments at Checkout.com. Picture this a seller in one country, a buyer in another, and a marketplace connecting them—taking a cut. This experience opened my eyes to fintech infrastructure. The Fintech Trifecta: Cheaper, Faster, Simpler Fintech revolves around moving money efficiently. Venture capital investment theses in fintech universally revolve around three core principles: cheaper, faster, and simpler solutions. Whether it's c

Announcements

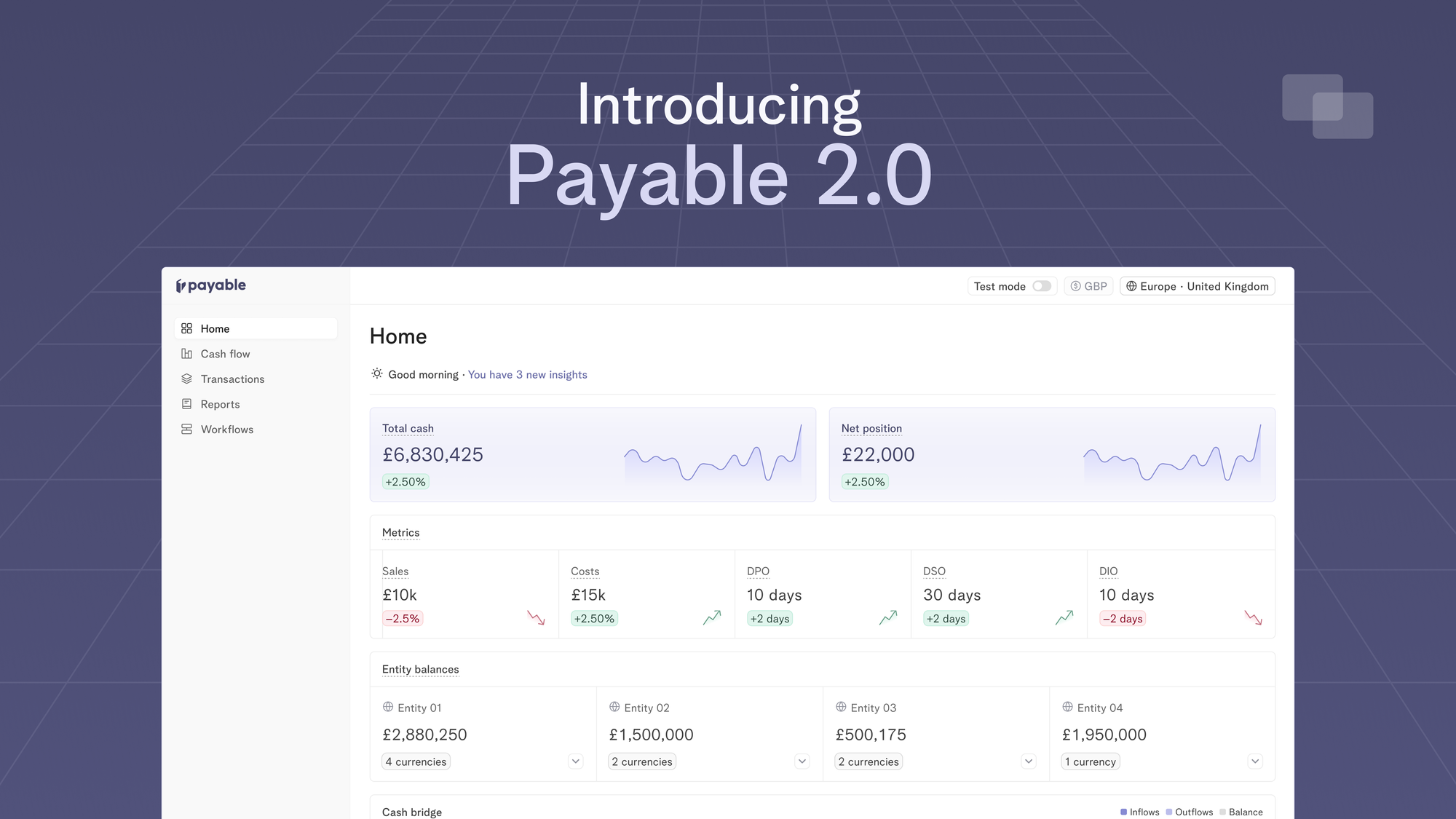

Introducing Payable 2.0 - one platform to optimise working capital, make fast liquidity decisions and move your cash metrics in real-time

13 Apr 2024

Today, we’re excited to launch Payable 2.0 which is our evolution to a more connected, intelligent and automated platform for finance teams to track their cash flows in real-time.